Mortgage calculators at your fingertips!

A multitude of calculators for you to figure out your details: Mortgage Calculator, Purchase Calculator, Land Transfer Tax Calculator, Debt Ratio Calculator, Closing Cost Calculator, and more.

Elevate your planning.

Secure Your Pre-Approval

Ready to make a move? Complete our secure, comprehensive digital application to obtain a formal pre-approval. This is the vital first step to lock in your rate and shop with total confidence.

Start My Application

Safety First

The Mortgage Stress Test

If you have bought a home in recent years, you should know about the mortgage stress test. It’s a test to keep Canadians from overextending themselves. Currently, you must qualify at the higher rate (5.25%) or your rate plus 2%.

Each December, OSFI decides if it will change the MQR. While it stayed at 5.25%, with fixed rates in the 4-5% range, the “+2%” rule is what actually impacts most buyers now.

Our calculator handles this logic automatically so you see your real qualifying power.

Analysis

Side-by-Side Comparison

Mortgage Rates: Compare two rates (like 4.49% vs 4.19%) to see exactly how much interest you’ll pay over the term. The app clearly spells out the savings from one option to the next.

Insured vs. Conventional: Compare 10% vs 20% down. See how much you save in interest by putting 20% down, while the app automatically factors in the default insurance for the 10% option.

Amortization: Compare 25 vs 30 years. A 30-year term offers more affordable cash flow but costs more in interest. Now you can see precisely how much that extra 5 years will cost you.

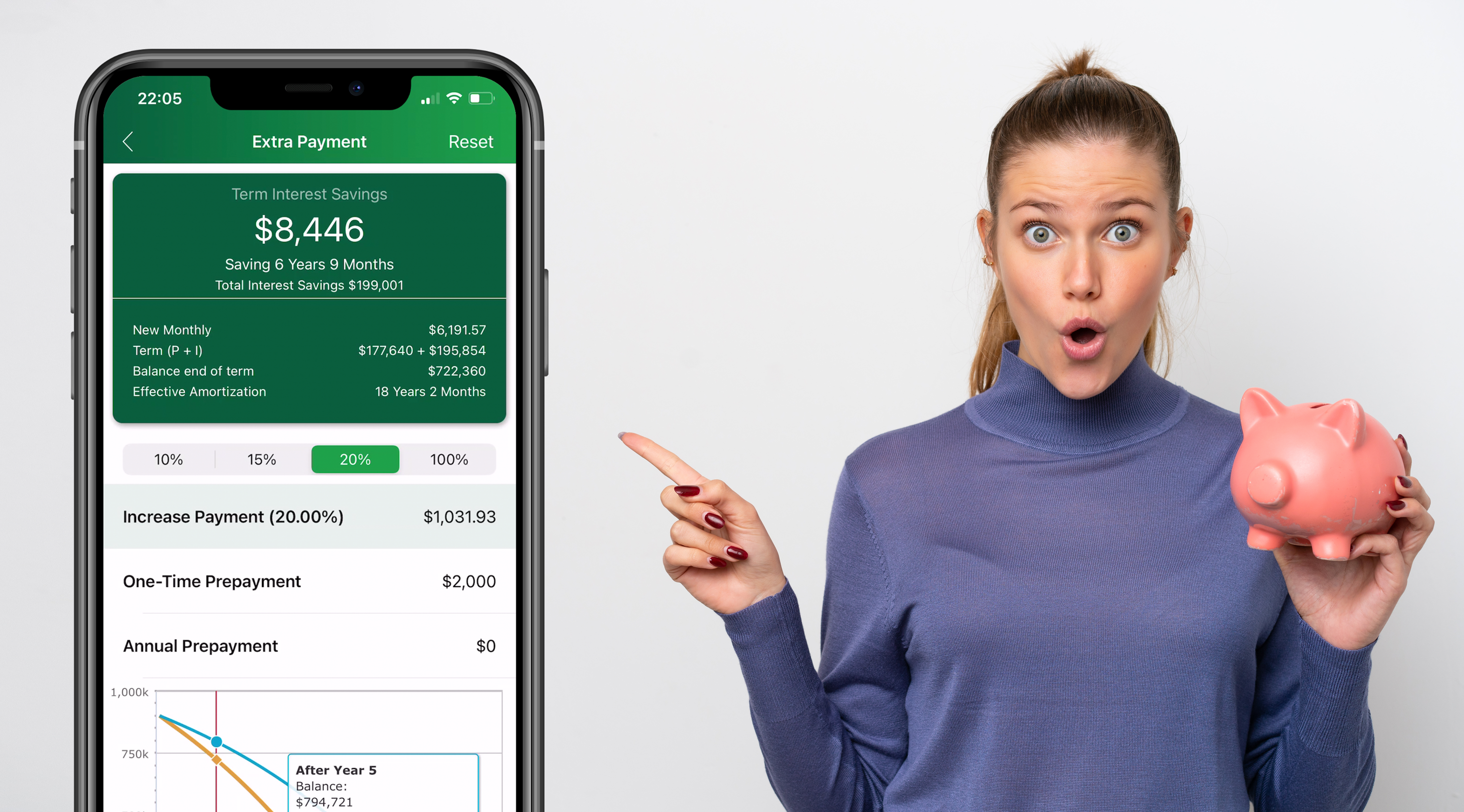

Wealth Strategy

Paying Your Mortgage Sooner

Increase your return by putting extra money against your mortgage rather than a low-interest savings account. Three ways to save:

- • Increase Payment: Extra money goes entirely toward the principal automatically.

- • One-Time Payment: Apply bonuses or inheritances directly to the balance.

- • Annual Prepayment: Use recurring funds like tax refunds to chip away at your principal every year.

Mortgage calculators at your fingertips!

A multitude of calculators for you to figure out your details: Mortgage Calculator, Purchase Calculator, Land Transfer Tax Calculator, Debt Ratio Calculator, Closing Cost Calculator, and more.