Fixed Rates & Bond Yields: The 3 W’s

“The Bank of Canada cut the rate, so my fixed-rate mortgage should drop today, right?”

Real Talk: This is a myth.

But, Why?

While the Bank of Canada controls the overnight rate (impacting variables), fixed rates are based on Bond Yields.

As you can see in the chart, even when the BoC announce cuts, the bond yield can actually rise. This divergence is why fixed rates often stay stubborn even when the news cycle sounds positive.

View Live Canadian Bond Yields →

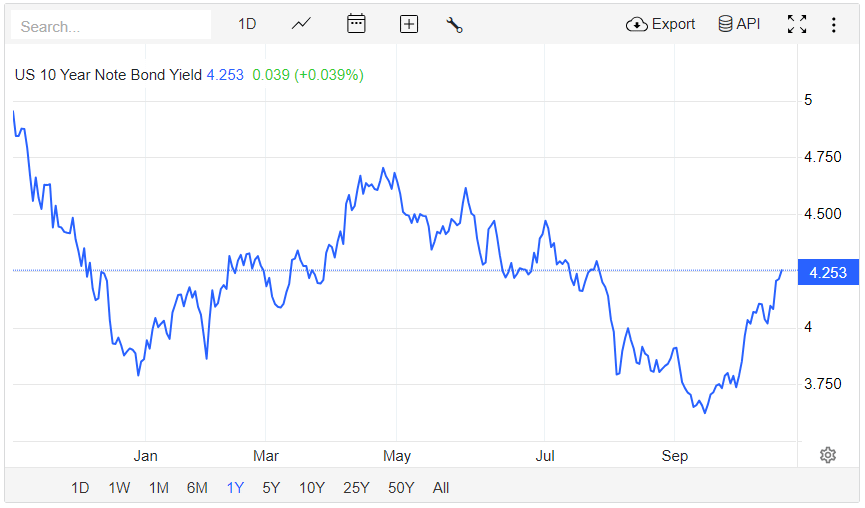

The US Influence

There is a loose correlation between our 5-year bond and the US 10-year Treasury. Because our economies are so tightly linked, our bond market often reacts to US economic data (like inflation or employment) before it reacts to anything domestic.

Looking at these two charts side-by-side over the year, the patterns are nearly identical. If you want to know where your renewal rate is going, you have to look South.

Fixed Rates & Bond Yields

A common misconception is that Bank of Canada (BoC) announcements dictate all mortgage rates. In reality, if you have a fixed-rate mortgage, those BoC meetings are often moot for your specific rate.

Fixed rates are driven by Government of Canada 5-year Bond Yields. These yields react to global economic factors—specifically US economic data like 10-year Treasury yields and employment numbers. Because our economies are so intertwined, when US yields move, Canadian yields often follow suit, regardless of what the Bank of Canada is doing with the overnight rate.

My renewal is soon – what do I do?

In a 2026 market where many are renewing from pandemic-era lows, your choice comes down to Peace of Mind vs. Market Timing.

Many homeowners are currently taking 3-year fixed terms. This provides immediate stability while betting that by 2029, the market cycle will offer even lower rates. A 5-year fixed remains the gold standard for budget certainty, locking you in for 60 months so you don’t have to think about a mortgage for nearly half a decade.

Personal Take: Having managed both fixed and variable payments, I prefer fixed for my own renewal. Even if payments stay static, I dislike watching my amortization stretch out to 60+ years when rates fluctuate. I’ll be taking a fixed for my next renewal to keep my timeline on track.

When is Variable your “Best Buddy”?

A variable rate mortgage can be a winning strategy when the Bank of Canada is in a holding pattern or a cutting cycle. Your interest drops automatically as the BoC cuts the overnight rate, meaning your monthly payments could get cheaper over time.

The Safety Valve: Remember, you can typically convert a variable rate into a fixed rate at any point during your term. If you take a variable now and fixed rates fall significantly in 12 months, you can lock into that lower fixed rate then, rather than committing to today’s pricing.

It’s all about your comfort level and how long you plan to stay in your home. If you’re comfortable riding the waves, the variable rate can really pay off over the long term.