Borrowers may have welcomed recent rate cuts from the Bank of Canada, but TD Bank and CIBC predict an additional 175 bps of easing by the end of 2025, lowering the overnight rate to 2.75%.

Optimism Among Borrowers: Big Banks’ Rate Predictions

As borrowers navigate the current lending landscape, many are placing their hopes in the forecasts provided by TD Bank and CIBC. Both institutions predict that the Bank of Canada will lower rates by an additional 175 basis points (bps) by the end of 2025.

What This Means

If these predictions come true, the overnight target rate would drop to 2.75%. This figure falls comfortably within the Bank of Canada’s neutral range of 2.25% to 3.25%, marking a level not seen since early 2022.

Comparing Predictions from Major Banks

When we compare predictions from the Big 5 banks, TD and CIBC’s forecasts stand out as particularly ambitious. Here’s a snapshot of other major banks’ expectations:

| Bank | Predicted Overnight Target Rate by End of 2025 |

|---|---|

| TD Bank | 2.75% |

| CIBC | 2.75% |

| BMO | 3.00% |

| Scotiabank | 3.25% |

| RBC | 3.00% |

Avery Shenfeld from CIBC notes, “An economy at full employment and on-target inflation theoretically requires interest rates to be at a neutral setting, which the Bank (and CIBC) see at 2.75%. Barring an economic shock, that’s a reasonable forecast for where 2025 will end up.”

The Easing Cycle

Shenfeld also emphasizes that the Bank of Canada will likely proceed cautiously during the current easing cycle. Rate pauses may occur between cuts, responding to economic data that could warrant a reassessment.

“As we’ve seen in the CPI news, economic data don’t follow a straight-line path,” Shenfeld explains. “Such pauses are more likely if there is a significant upside surprise in employment, growth, or inflation.”

The Key Indicator: Inflation

In an inquiry regarding TD’s forecast, senior economist James Orlando stated, “I think inflation is the main indicator to watch. That and a continued confirmation of economic weakness.”

So far, these observations align with what the Bank of Canada has been experiencing, reinforcing the importance of closely monitoring inflation trends as we move forward.

In conclusion, as we await the Bank of Canada’s decisions, the forecasts from TD Bank and CIBC provide a glimmer of hope for borrowers seeking relief in the coming

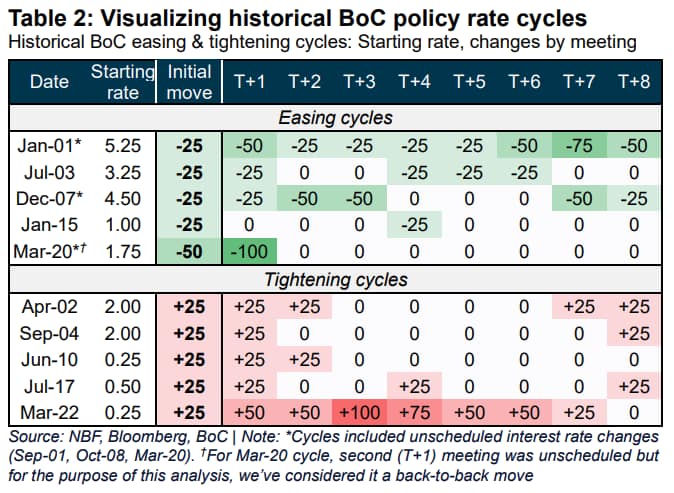

A history of BoC rate cuts

During the 2001 easing cycle, the Bank of Canada implemented a series of 11 consecutive rate cuts, bringing the overnight rate down from 5.75% to 2.00%. This represented a substantial total reduction of 375 basis points over a span of 12 months.

Context of the Rate Cuts

This swift and significant decrease in rates was part of the Bank’s strategy to mitigate the economic slowdown that followed the dot-com bubble burst and the repercussions of the September 11 attacks.

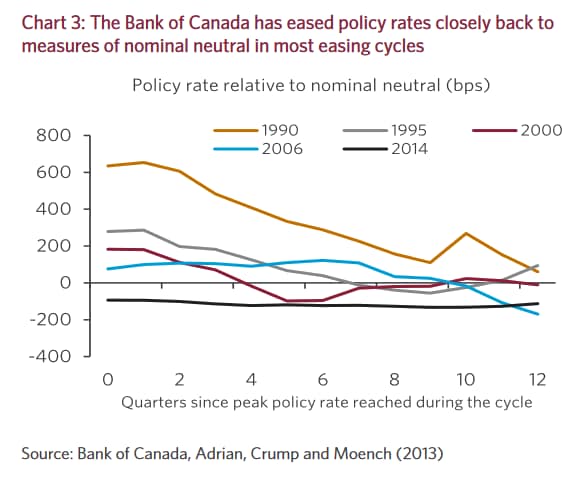

Historical Perspective on Easing Cycles

According to CIBC, in most prior easing cycles, the Bank of Canada typically adjusts its policy rate back to a neutral level within one to two years. The only significant deviation from this pattern occurred during the 2014 oil price shock, where rates remained below neutral for an extended period.

Avery Shenfeld from CIBC explains, “Canadian real rates tend to gradually move towards or stay close to the neutral rate in soft landings, while in the U.S., there are more abrupt adjustments due to hard landings.”

Understanding the Differences

These variations may reflect the greater sensitivity of the Canadian economy to high interest rates, necessitating a quicker return to neutral territory when signs of economic slowing emerge. This approach is crucial in efforts to prevent a recession.

As we reflect on these historical trends, it’s clear that the Bank of Canada’s strategies in previous easing cycles can provide valuable insights into potential future actions as economic conditions evolve.