As of October 23rd 2024, Canada’s prime lending rate is now 5.95%! That’s a 50 basis point drop!

The bond yield on the 22nd was trending upwards for no apparent reason, but maybe now with this overnight rate (and therefore prime rate) decrease it will help the bond reverse directions!

That being said, this article in the Financial Post explains the outcomes to expect with a 50bps october rate cut:

- Floating-rate borrowers will feel like they’ve won a mini-lottery. With the average Canadian’s mortgage debt around $300,000, variable-rate mortgagors’ will find another $30 per $100k of mortgage back in their pockets each month, depending on their loan type (fixed payment vs floating payment). That’s money most can use to pay down debt or buy necessities without incurring more debt. Others will use it to finance discretionary purchases. Such spending sprees eventually spawn new jobs and added inflation.

- Incrementally more homebuyers will rush to open houses this october and november on the belief they now qualify for a mortgage or need to beat the crowd. Ultimately, however, falling rates will have their anticipated effect, making homebuying more budget-friendly — at least temporarily. For now, the effect will be largely psychological, unless there’s a drop in the government’s minimum qualifying rate (MQR). That’s the rate banks make mortgage applicants prove they can afford. For the MQR to fall, fixed rates need to drop, and that depends on how much more rate-cutting the market anticipates after Wednesday.

- A 50 basis point cut would slash the average new conventional floating-rate mortgage from 5.60 per cent (prime minus 0.85 per cent) to 5.10 per cent. That’s about $30 in monthly savings per $100,000 borrowed — enough for a fancy coffee habit or a subscription to yet another streaming service you’ll never watch. It will also slash the annual income required to qualify for that variable mortgage by roughly $5,000, to $117,000 on a 30-year amortized $500,000 mortgage (assuming a well-qualified borrower has no other debts). That means, for some, their dream home might be less “dream” and more “attainable reality.”

- Canada’s beloved loonie — which moves largely on U.S.-Canada interest rate differentials and energy prices — could take another hit (sorry, snowbirds). That could jack up the cost of foreign goods and services. Such imported inflation could potentially lessen the need for further rate cuts.

- If inflation creeps higher in the next few months, expect economic pundits to question if the Bank of Canada has gone overboard with monetary easing. Rate cut expectations could then fizzle a bit, especially since North American labour markets and spending are still perky. That’s why a significant minority of Bay Street number-crunchers are advocating for a more cautious approach to monetary policy easing.

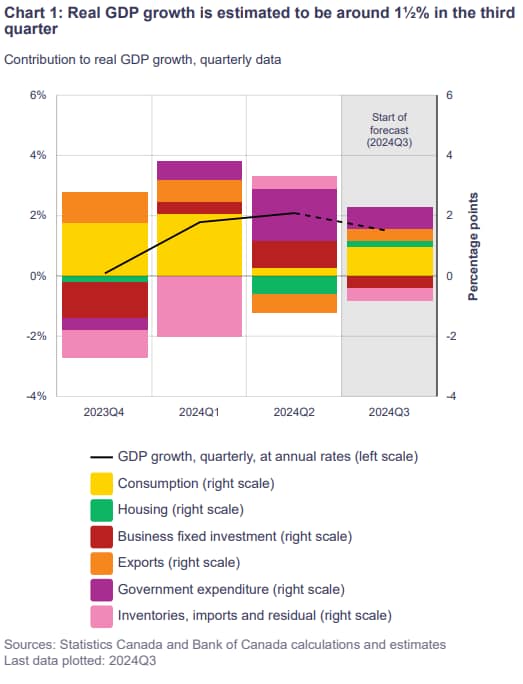

An interesting chart from the report this morning specifically talking aout the GDP and what the makeup of the growth is expected to be over the next few months

Want to see previous interest rate annoucements from 2024?

Want to see when the annoucements are in 2025?

Want to read the release directly from the Bank of Canada themselves?